"In the age of instant QR payments, the 'Convenience Tax' is real. While UPI is great for chai, it’s a disaster for your wallet on big-ticket items. We break down the 2026 'Reward Stacking' blueprint that beats UPI every single time on Amazon, Flipkart, and Myntra."

The Convenience Trap: Scanning Your Way to Zero Savings

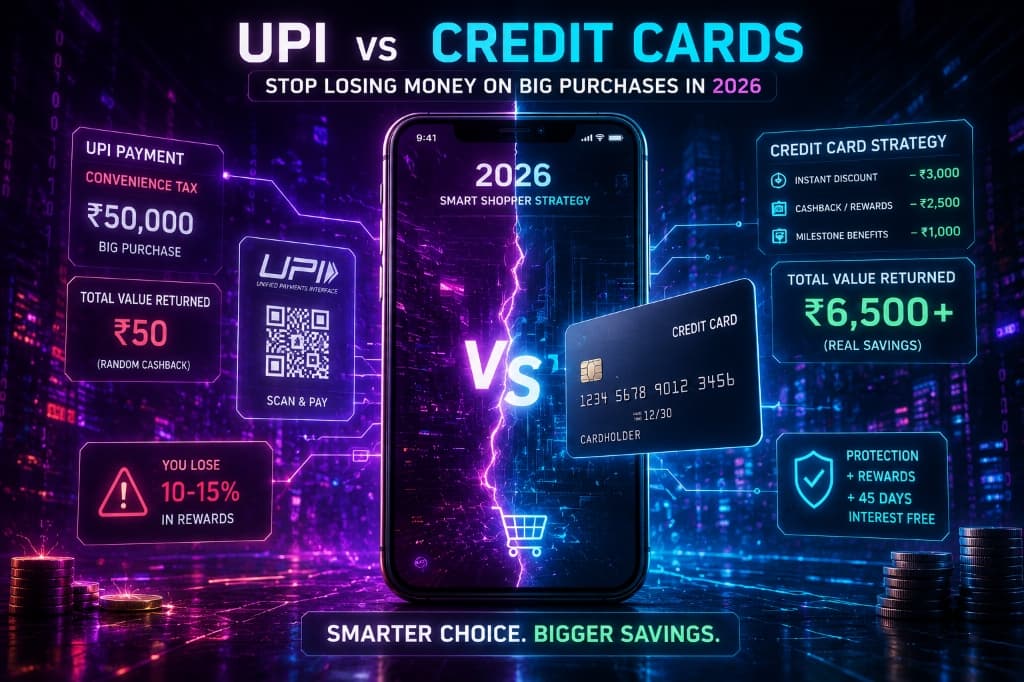

In 2026, scanning a QR code is second nature for every Indian. But after analyzing thousands of transactions, the data is clear: Using UPI for any purchase over ₹2,000 is a strategic mistake.

When you use UPI for a ₹50,000 iPhone, you get a 'Scratch Card' worth ₹2. When you use a strategic Credit Card, you get an immediate ₹2,500 to ₹5,000 in value. That difference isn't just 'points'—it's real money that pays for your next year’s Prime or Plus membership.

The Math: UPI Convenience vs. Credit Card Strategy

Let's compare the value returned on a typical monthly 'Loot' spend of ₹40,000 (Electronics, Fashion, and Groceries):

| Benefit | UPI Payment | Strategic Credit Card (e.g., SBI Cashback) |

|---|---|---|

| Cashback | ₹0 - ₹50 (Random) | ₹2,000 (Flat 5%) |

| Bank Offer | Rare (1-2%) | Instant 10% (During Sales) |

| Protection | None | Fraud/Chargeback Protection |

| Interest | Money leaves bank now | 45-50 Days Interest-Free |

| Total Value | ~₹50 | ₹6,000+ (During Sale stacking) |

The Verdict: By using UPI, you are effectively paying a 10-15% 'Ease Surcharge' on every major purchase.

The 'Triple-Stack' Blueprint for 2026

To truly maximize your savings, you need to master the Triple-Stack. This is how pro-shoppers get flagships for effective prices lower than MSRP:

- The Base Discount: Wait for the platform price drop (Amazon GIF or Flipkart BBD).

- The Instant Bank Offer: Use the partner card (e.g., SBI for Amazon) for the immediate 10% off.

- The Reward Accelerator: Ensure your card gives 'Default Rewards' on top of the instant discount (cards like the Amazon Pay ICICI or Axis Flipkart are king here).

Pro Tip: In 2026, some platforms have started allowing 'UPI on Credit' via Rupay. While convenient, the rewards are often slashed. Always prefer the Physical/Online CC path for maximum points.

Safety First: The 'Chargeback' Shield

One major reason to advocate for Credit Cards over UPI for big loots is security. If you pay via UPI and the seller sends you a stone instead of a phone, getting your money back is a nightmare.

With a Credit Card, you have the power of Chargeback. You can dispute the transaction with your bank. The bank blocks the payment to the merchant until the issue is resolved. This 'Consumer Shield' is the biggest reason why smart shoppers use plastic for high-value items, not just QR codes.

Top 3 'Value-King' Cards to Carry in 2026

If you don't want a wallet full of cards, just get these three:

- SBI Cashback Card: The undisputed heavyweight. Flat 5% on almost all online spends. No BS, just cash in your statement.

- HDFC Millennia / Swiggy: Perfect for the urban Indian. High cashback on food, travel, and shopping.

- Amazon Pay ICICI / Axis Flipkart: The 'Ecosystem Kings'. Essential if you do 80% of your shopping on one specific platform.

Final Verdict: The Smart Shopper Strategy

Use UPI for your milk, your chai, and your local kirana store. It’s the best tool for micro-payments. But for everything else—anything that adds value to your life or costs more than a meal—think strategically. Use the credit cycle, stack the rewards, and keep that extra 10% in your own pocket.

Don't let the convenience of a QR code blind you to the thousands you are losing every year.